Know If You Can Retire… Without Paying 1% Fees

Our Hourly, Fee-Only Financial Planning model allows you to gain financial clarity without the conflict of commissioned sales or paying 1% of assets managed.

Most of our clients were making good money decisions before they started working with us. If you are like most of our clients…

You won’t hire a financial planner to pick the ‘right stock or mutual fund’. You recognize the lack of value in that venture (especially in the long run).

You understand other choices (cash flow, taxes, etc.) have a greater impact and more importantly, you have more control over those decisions.

You are not looking for a crystal ball. You are looking to gain clarity and confidence about your financial future (and the decisions along the way).

You aren’t looking for a sales pitch. You aren’t looking for someone to ‘take over’. You are looking for informed (non-emotional) guidance. You might call it a second opinion.

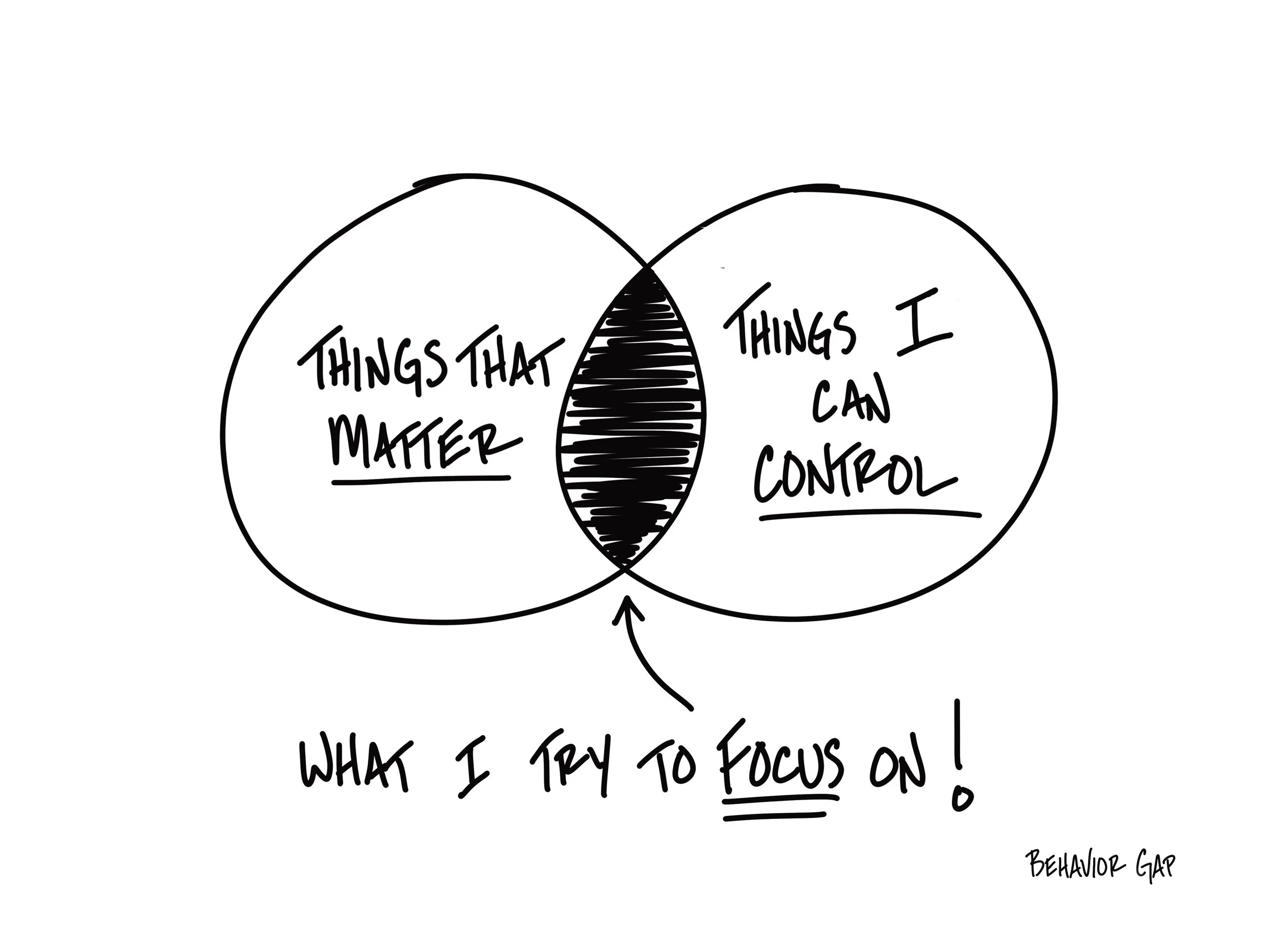

We believe there are two reasons to hire a financial planner.

The first is to remove (or at least lessen) the emotions often attached to money.

The second is to gain the experience of what other people did (both good and bad).

The ultimate goal is to help you build a foundation (or roadmap) from which you’ll make informed money decisions going forward.

Three common misconceptions about working with a financial planner.

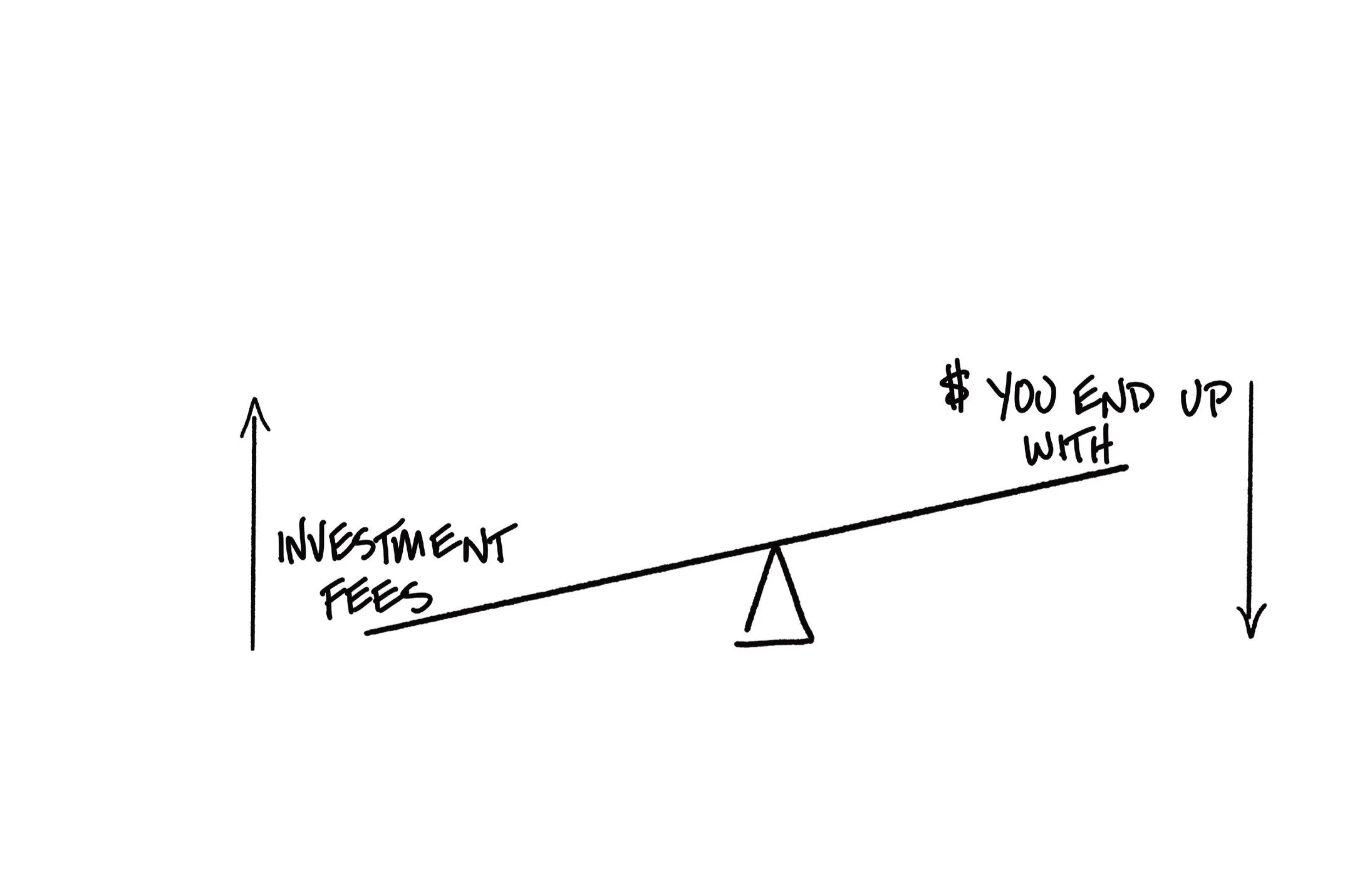

All advisors sell commissioned products (or charge 1%). NOT TRUE!

Our fees are based on hours; we don’t sell commissioned products… or charge 1% to manage assets.

You need to have ‘a lot of money’ to work with an advisor. NOT TRUE!

There are multiple components of your retirement plan beyond how much money you have that determine success.

I’ll have to give up control of my investments. NOT TRUE!

Over 50% of our planning clients continue managing their own assets (with increased confidence). If you choose to have investments managed, the fee will be based on hours- not the typical 1% (or more) annual fee.

Achieve Financial Peace of Mind With Ongoing Support

Build a plan tailored to you!

A financial or retirement plan should be based on the specifics of your values, goals, and motivations. We’ll take the time to know what is important to you.

Enjoy confidence in your retirement readiness!

When you have a clear path towards retirement success, you also gain the confidence to enjoy today.

Gain ongoing support

Our hourly fee structure allows various ways to gain ongoing support. If you prefer to invest your assets, you can, and still have ongoing support.

Simple, Transparent Fee Structure

Our fee structure is simple. Our hourly fee is $250 per hour. We do not earn income from any other source. We believe this best serves our fiduciary duty and aligns with how most other professionals are compensated.

-

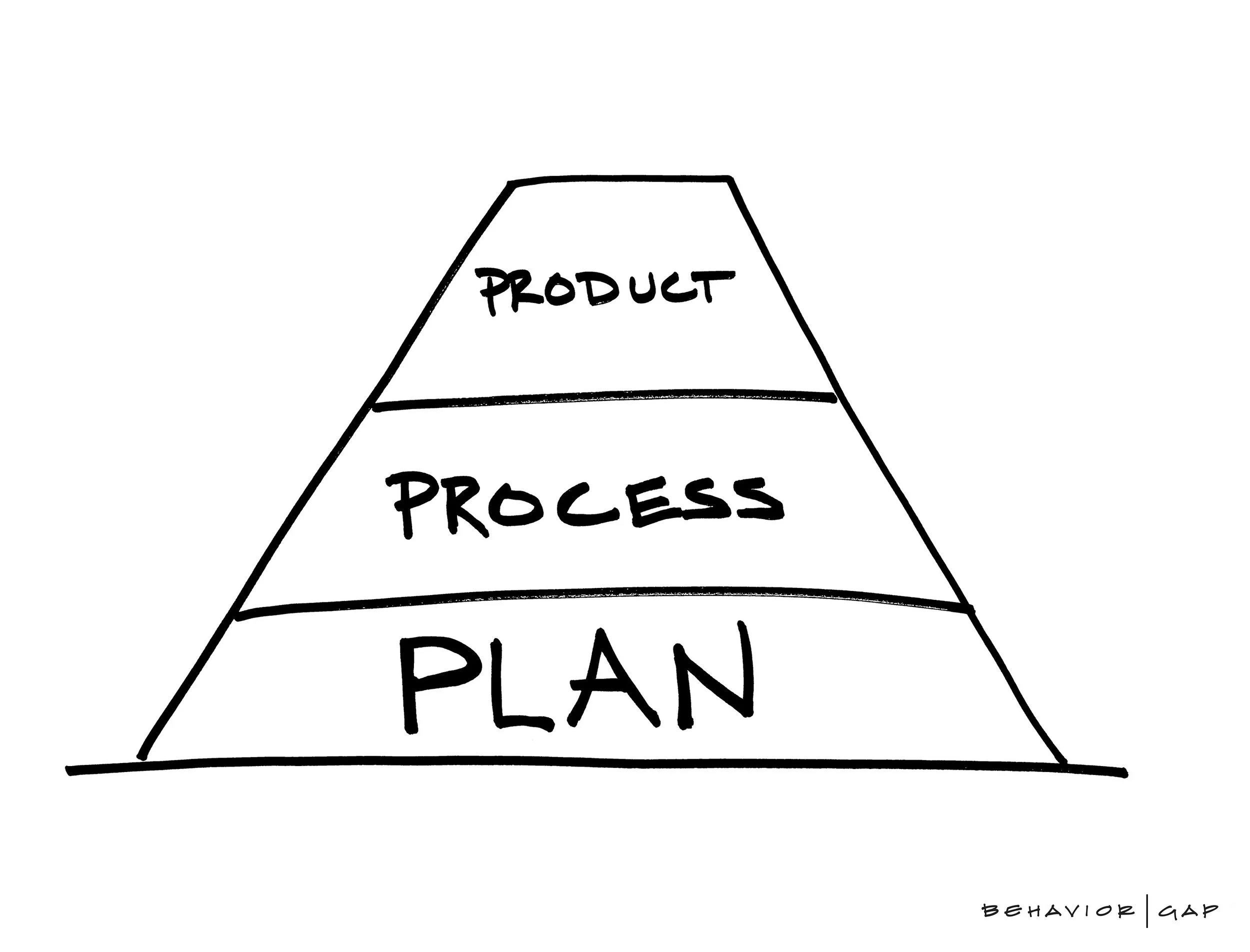

Starts with a plan

We begin with the creation/review of your existing plan.

The initial planning fee is based on the complexity of your situation.

Most plans require between six ($1,500) hours and ten hours ($2,500).

During the intro discussion, we’ll get a better idea of your situation.

-

We Manage Your Investments

After a plan is created, you may prefer to have us manage your investments.

We’ll discuss the reasons why you may want to have ongoing investment management.

Fees are based on hours rather than a percentage of assets.

The range is typically between $500 and $1,000 per quarter ($1,000 and $4,000 annually).

-

You Manage Your Investments

You prefer managing your investments or most of your investments.

You aren’t ready (or have the need) to relinquish ongoing management, but you’d like to update your plan from time to time. No problem…

We’ll update your plan and address questions/changes based on an hourly rate. Most plan updates range between $500 and $1,000.

The Initial Planning Process

Meet to discuss the specifics of your specific scenario

During our interview, we’ll discuss what is important to you when building a financial future. We’ll share our model (different from most). If we agree working together makes sense, we’ll move onto the next phase.

Create a plan

Our planning process consists of three meetings.

Intention Meeting. We’ll review your current situation and consider/discuss your desired outcome. We’ll answer the question most want to know…”will you fail retirement?”. After sharing the initial info, we’ll send you home to consider what you might change after seeing the results (spend more/less, travel more/less, retire sooner/later). By the way…there are two ways to fail retirement…having too little or having too much!

Attention Meeting. Typically begins with scenarios you want to 'test’ after seeing the original outcome. We dig into details. We consider what could go wrong and consider opportunities. Tax planning and cash flow planning are frequent discussion points in this meeting. We’ll also discuss investments (down to the fund level).

Guidance/Repetition Meeting. We’ll provide a written draft of your plan for review prior to the meeting. We’ll discuss and adjust the plan as needed. The ultimate goal of this meeting and the process in general is to provide a clear roadmap for how and more importantly why we recommended what we did. In most cases, we can narrow the steps into three to four simple repetitive steps (automated when possible).

Ongoing Management or Hourly Updates?

With a plan in place, you decide if you prefer to continue managing your portfolio or prefer that we do. We’ll discuss how either solution works. You decide what is best for you. Over half the people we write plans for continue to manage their investments (with some new guidance).

A solid foundation supports retirement success.

At its core, a financial plan is simply a summary of what you earn, spend, save, and protect.

The question is not whether you have a financial plan. The better question is whether your current plan is likely to produce the results you want.

Having a solid understanding of your current and projected financial future provides a solid foundation from which to make informed retirement decisions.